.svg)

Insight

Technology-neutral investment tax credits are now available for clean energy projects constructed or supplying energy in 2025.

Feb 3, 2025

Technology-neutral investment tax credits are now available for clean energy projects constructed or supplying energy in 2025.

Editor's Note: Since the OBBA was signed into law on July 4, 2025, there are new rules and timelines that impact the 48E Tax Credit. We recommend reviewing our recent post on the One, Big Beautiful Bill Act.

The IRS published its final rules for the Clean Electricity Investment Credit (IRS tax code section 48E) and its related Production Tax Credit (IRS tax code 45Y), effective December 12, 2024. These replace the technology-specific Energy Investment Tax Credit (section 48) and Renewable Electricity Production Tax Credit (section 45) which phased out at the end of 2024. The final rules update the proposed rules and guidance from the Treasury and IRS issued in November 2023.

Using 48E, investors in the development of qualified energy properties and facilities are eligible for a tax credit from normally 30% all the way up to 70% of the cost of the project (in extreme cases) through an Investment Tax Credit (“ITC”). 48E is just one of many clean energy spending and investment approaches signed into law with the Inflation Reduction Act (IRA) in August of 2022. It aims not only to support the energy transition to zero carbon emissions electricity, but also to simplify the framework for these projects to become eligible for ITCs.

Importantly, both 48E and 45Y are effective across a longer time horizon–extending through 2032–than the previous iterations of the investment tax credit. They also apply to the construction and energy production from a wider range of qualifying technologies and property types. The technology neutral focus allows more clean energy project developers and operators across more industries to qualify and consequently monetize their tax credits.

The longer time horizon from the IRA provided much-needed investment stability for industry: “By ending short-term legislative extensions for the ITC, the Inflation Reduction Act (IRA) has given clean energy project developers clarity and certainty to undertake major investments,” said Wally Adeyemo, US deputy secretary of the Treasury.

In this article, we focus on the ways 48E differs from previous ITC iterations. The 48E credit extends many previous provisions for technology-specific ITCs, but are summarized below.

One of the most important changes brought by the 48E investment tax credit and its closely related 45Y production tax credit is "technology neutrality.” Previously, the ITC under section 48 only applied to specific emissions-free technologies such as solar and wind power resources. Now the floodgates have burst open for a wider range of zero emissions technologies to receive ITC-driven investment opportunities. Several key benefits come from this change.

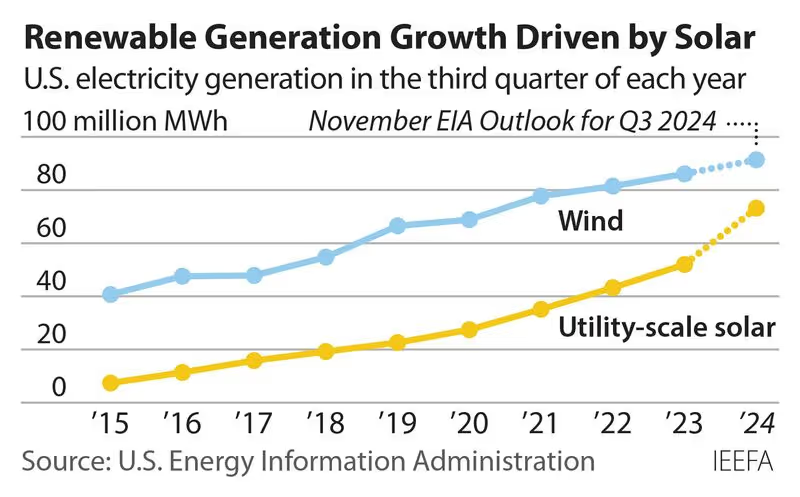

The U.S. launched its first ITC in 1978, with a 10% tax credit for wind and solar resources, and its various iterations have expired and been extended with Congressional approval for several decades. Its most notable prior upgrade came with the The Energy Policy Act of 2005, when its value increased to 30% of a system's cost, and added 30% residential system ITC. Growth in solar and wind generation has steadily increased parallel to the availability of ITCs. Utility-scale solar generation in the U.S. has grown 838% over the past decade.

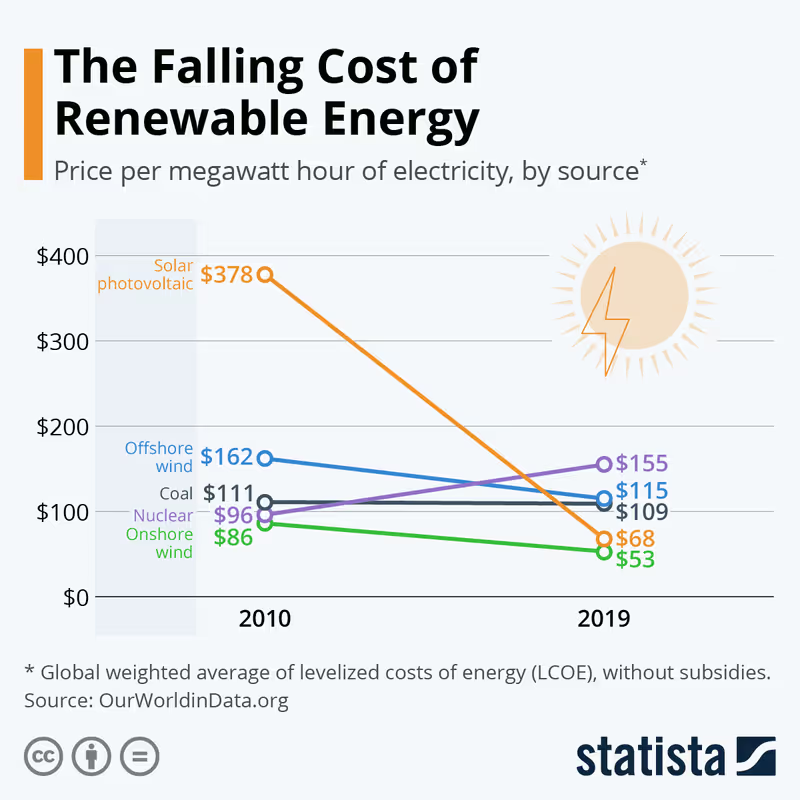

Solar and wind also experienced significant declines in the cost to produce renewable energy.

With a long-term policy signal available for investment into a wider range of clean technologies and systems, more industries could follow a similar growth and cost reduction trajectory. Some of the clean electricity industries with the highest levelized cost of energy include offshore wind, battery storage, and biomass.

Expanding the range of clean electricity sources in the U.S. could help meet growing demand for electricity and improve reliability. The U.S. Department of Energy forecasts electricity demand growth of approximately ~15-20% in the next decade, with the potential to double by 2050. The increase is driven in part by the shift towards electrification across the transport, building and industrial sectors as a key energy transition strategy. Growth in high energy consuming data centers supporting AI and expanded U.S. manufacturing and industrial growth have also contributed to electricity demand increases.

Clean electricity diversification is important for meeting demand and ensuring grid reliability. Decentralized sources of electricity and energy storage solutions are important for balancing grid demand and supply as the grid increasingly relies on intermittent renewable energy sources. The ability for large energy consumers like commercial buildings to switch off of grid-dependent energy sources at a moment's notice helps utilities to avoid firing up high carbon emissions energy sources during demand peak events.

48E creates a longer time horizon for project development, applying to projects placed in service after December 31, 2024 and extending to either 2032 or when U.S. greenhouse gas emissions from electricity reach 25% of 2022 emissions or lower: whichever comes later. Per the 2032 timeline, phase out would begin in 2033, reaching 0% in 2035.

This long timeline is important for achieving climate-related energy transition goals. There is no clear reason for incentives to drop off before achieving significant absolute carbon emissions reductions in the U.S. Transitioning energy infrastructure requires reliable long-term financial incentives for feasibility. With this extended timeline, the U.S. has indicated the energy transition is here to stay.

The longer time horizon marks an important shift from prior policy approaches. The IRS recalled in its request for comments on 48E: “Congress has repeatedly amended § 48, including repealing and suspending the credit, changing the amount of the credit and rules for eligibility.” This history of amendments created confusion and uncertainty for project developers and investors, pausing or cancelling many projects that would have contributed to a cleaner generation mix in the U.S.

Even though 48E was passed as part of the IRA, which may contrast with the incoming Trump administration's policy agenda, it would be challenging to amend or repeal due to continued bipartisan support for the IRA. This is largely because the IRA supports job creation, manufacturing and other important economic development in Republican-led regions of the U.S.

While there's potentially a risk that spending specified in the IRA could be at risk of reduction through budget reconciliation, the long-standing success of the ITC would also potentially make it less of a target than other parts of the IRA. It aligns with Trump's general support for lowering the tax burden on corporations and includes tax credit eligibility for carbon capture and storage facilities, largely favored by the fossil-fuel energy industries as a means to offset emissions.

In spite of covering a wider range of technologies, justifying qualification for unique projects could become an issue. For each technology, specific issues determining qualification still apply. Many of these issues were clarified by the IRS, in response to 350 comments received from stakeholders.

The IRS's final rules for section 48E clarify the definitions of property eligible for the ITC, informed by 350 written comments from stakeholders. Here are some of the technology-specific issues addressed in the final rules.

We recommend a third-party consultation for accessing tax credits for investment in energy projects with uncommon technological features or potential for not meeting greenhouse gas emissions requirements. Basis can provide direct consultations or identify a relevant advisor in these cases. Get in touch.

Related resources: Department of Treasury press release; IRS Clean Electricity Investment Credit page; IRS § 48E; Columbia University Inflation Reduction Act analysis